Perfect Storm of Trade Wars and Cold Wars Will Drive the Gold Price Higher

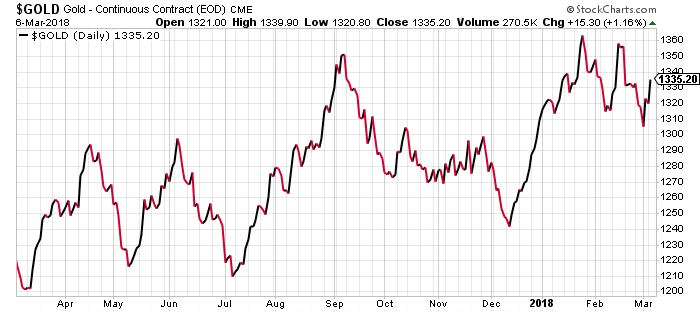

The gold price has started to recover, posting strong gains on March 6. The gold price per ounce has finally reversed the bearish trend that began in the second half of February to reach $1,332. This increase is at once surprising and anticipated.

The gold price has increased in parallel with the U.S. dollar. The dollar has posted some minor gains against the euro. Despite the European currency’s continued resistance, there are heavy risks ahead, which could hurt the dollar and favor gold.

Advertisement

The Italian election has resulted in the victory of anti-eurozone and anti-immigration (or at least in favor of much tougher immigration rules) parties. The tandem rise of gold and the dollar suggest that there’s a real danger of collapse for the European currency.

But if the dollar hasn’t scored big gains after such a significant shift in what was one of the most pro-European Union (EU) countries until not so long ago, it points to a bigger issue. There’s a resurgence of the kinds of risks that make gold the safe asset that it has always been. The fact that gold has gained over two percent in March after a dollar rebound (however minor it may be) may herald a more bullish course for the yellow metal in 2018.

Federal Reserve Chair Jerome Powell recently hinted what Americans can expect for interest rates in 2018: at least three or four increases. Normally, that would put downward pressure on the gold price. Instead, a reversal of the expected trend is happening.

The stronger dollar (or, at least, its anticipation) was supposed to work against pundits projecting higher gold prices. The market has already enjoyed the time necessary to absorb this since January, when a favorable jobs report was issued.

Thus, as Powell dropped hints that he would oversee as many as four rate hikes in 2018, the market had already digested this. Therefore, when Powell makes these hikes formal, the market’s reaction will be mild—unless Powell pulls off a stunt, raising rates much more than the hinted 0.25%.

At This Point, It’s All About Gold

The market and the dollar have already absorbed the potential value-enhancing circumstances. As for the factors that will push the gold price higher, they’re just warming up. But at this rate, the gold prospects are heading toward red-hot.

Chart courtesy of StockCharts.com

Many had forgotten about Donald Trump’s isolationist and protectionist electoral promises. Good or bad, he has shown that he’s willing to fulfill his program. He has passed tax cuts, as flawed (or even disastrous) as they might prove in the long run. President Trump has also officially recognized Jerusalem as Israel’s capital.

Thus, it should come as no surprise that the Trump administration has now decided to tackle trade deals—or, rather, dismantle trade deals. By 2019, the North American Free Trade Agreement (NAFTA), one of the pillars of the North American economy (Canada, Mexico, U.S.) will either have met its demise or present substantial differences to the present accord.

The NAFTA earthquake has begun. Trump has announced that the United States will start to impose substantial duties on steel and aluminum imports. The U.S. imports most of its aluminum from Canada; therefore, NAFTA will be involved. While trade and foreign affairs officials work out the various difficulties that Trump’s decision implies, investors can expect two things: added volatility in the equity markets and unexpected support for higher gold prices.

There’s Nothing Normal About the Trump Era

Ultimately, however, gold prices are going up simply because there’s nothing normal about our times. And that might be bad for predictability and stability. Despite what the pundits have been propagandizing about Russia and Vladimir Putin, the evidence gathered to build the Russian electoral meddling case is flimsy and illogical.

Nobody has yet to explain, even if the Russians used ads on Facebook (which appeared largely after the November 2016 vote), how on Earth that would have corrupted the vote any more than Americans have influenced elections in allied countries for decades—or any more than the U.S. influenced the 1996 elections in Russia.

But “Russiagate” is just one element. The more important one is the emerging Cold War, which will drive military spending to excessive heights. President Ronald Reagan diverted billions of dollars into nuclear armaments and researching the so-called “Star Wars” defense system. The idea was to use this, along with arming the Taliban/mujahedin in Afghanistan, to bankrupt the Soviet Union.

The technique partially worked. Soviet President Mikhail Gorbachev, who had a personal desire for better relations between the U.S. and the Soviet Union, no doubt had incentives to negotiate to slow the hemorrhaging of funds, which Moscow’s military equipment makers were consuming.

A New Cold War

Yet now, if Trump and the military establishment think they’re going to force Russia to give in to western demands on matters from Ukraine to Syria, they are heavily mistaken. The opposite may occur.

Putin recently delivered a speech announcing new Russian weapons that will make it difficult, if not unwise, for anyone to launch a major attack on his country. Whatever the U.S. and NATO have to launch against Russia, the latter can respond in kind and shoot it down. It would be suicidal, of course, for anyone to launch a first strike against Russia or one of its allies.

And note, Russia spends a fraction on armaments than does the United States. The best that Americans can obtain from the present Russian/West hostility is excess spending on military equipment.

Military spending is going to exacerbate U.S. debt. This will have the effect of rendering any Federal Reserve rate hikes more painful. More debt plus higher interest is never a good idea. The White House’s military grandstanding will end up costing Americans too much.

As for the tariffs and Trump’s protectionism, there are already internal obstacles getting in the way of the plan. Gary Cohn, Trump’s main economic advisor, has quit. Cohn’s resignation comes just days after Hope Hicks, Trump’s communications chief, also quit. Cohn was one of the chief architects of Trump’s tax reform.

Cohn, until recently, was a Trump loyalist. He quit in protest over the tariffs that Trump is planning to enforce on steel and aluminum. Trump has shown that he can act more controversially than even his advisors can sustain. Cohn, evidently, is not interested in starting a trade war. Whatever compromise Trump may have reached within his own team in the past few months is broken now.

The Effects of a Trade War

In November 2016, the markets had initially feared Trump’s win because of his threats to enforce trade restrictions and tariffs. The fears were easily quelled as Trump focused more on tax cuts, encouraging the bulls on Wall Street. Now, those initial fears will return and prey on an already shaky and uncertain market that fears interest rate hikes.

A perfect storm is coming that will hurt stocks and favor safe havens like gold.

Trump may want to protect American jobs and workers, but applying “you are with us or against us”-style policies to trade will be just as effective as such thinking has been for diplomacy. Expect a trade disaster.

The EU has promptly announced that it would react to any tariffs with countermeasures to be applied against U.S. manufactured goods, from Harley-Davidson motorcycles to specialty beverages and clothing like certain brands of jeans.

Then there’s China. Beijing has already warned Washington that it would take all measures to fight back against Trump’s protectionism. Apart from applying costs to certain U.S. imports—such as grain, for example—China can always start dumping U.S. dollar-denominated debt, of which it owns a considerable amount.

This would drive the value of the dollar down, making it more difficult for America to finance its military procurement (among other consequences).

On a more general scale, U.S. tariffs would act as a brake and an obstacle on global trade, which drives economic growth. Americans would also end up paying more for everything from groceries to cars. It would exacerbate already untenable income distribution disparities and destroy the retail sector (and subsequently, retail jobs) so dependent on consumption.

Ultimately, Trump’s trade restrictions would cause damages within and beyond the United States. In investment terms, the risks are, to use a Trump euphemism: huge.